2023 Annual summary –

the Swiss advertising market

written by CAO Tina Fixle

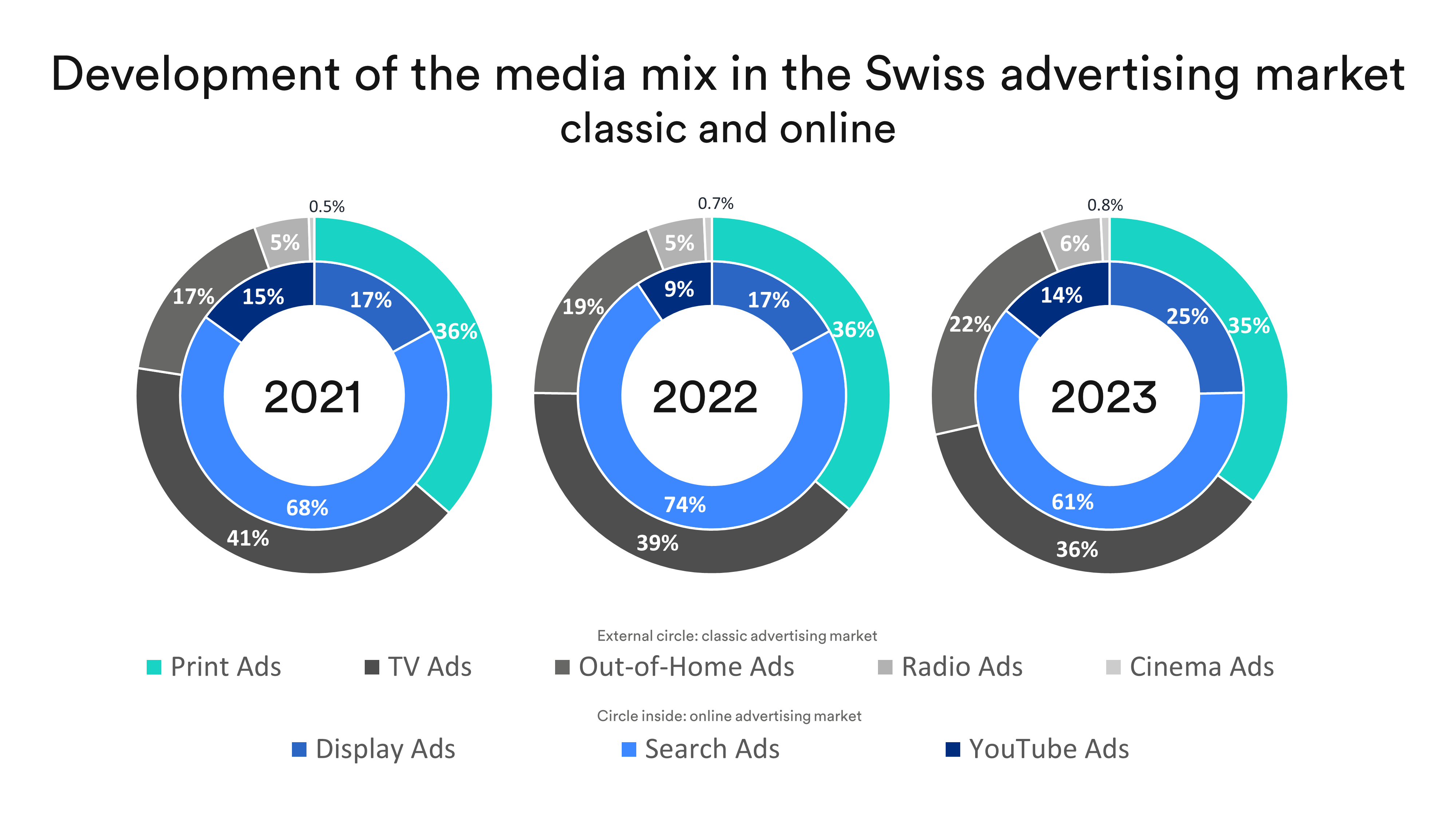

The “traditional” advertising market generated CHF 3.95 billion in gross advertising pressure in 2023. This represents a modest drop of -1.1%. Outdoor advertising once more enjoyed increased popularity (+16.3%), cushioning falls in TV (-8.3%) and print (-3.6%) advertising. Radio and cinema advertising also experienced growth (5.1% and 9.0% respectively), albeit to a much lower level in absolute terms. The order in Media Mix remained unchanged, although media did draw closer together: TV (36%; -3 percentage points) and print (35%, -1 percentage point) led the way, with out-of-home (22%; +3 percentage points), radio (6%, +1 percentage point) and cinema (0.8%) bringing up the rear.

Looking at the world of online marketing, display and YouTube ads (CHF 536 m (+4.7%) and CHF 305 m (+8.8%) respectively) saw strong upward trends, although no longer in the two-figure percentage range as in previous years. The figures make it clear that digital advertising formats are continuing to grow in importance, even though the rate of growth has slowed slightly compared to previous years.

In terms of search ads, a direct comparison with the previous year is problematic as a result of the ongoing changes and updates that Google carried out in the second half of 2023 in particular. These continuous changes, which were also documented in detail in the media, led to significant fluctuations in the search results. This means that a direct comparison with 2022 would not be meaningful. That said, 2023 itself does provide a basis for internal comparisons and analyses despite its momentum.

Coop, Migros and P&G set the course – not everyone follows

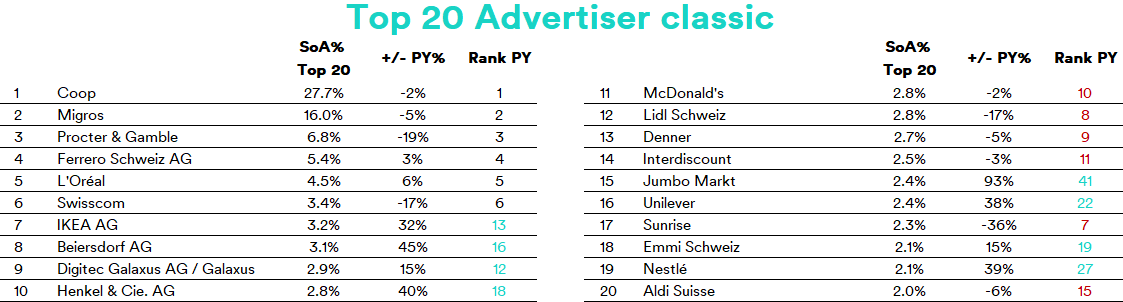

Coop (1) continues to hold the top position (SoA% top 20: 28%) with a slight year-on-year decrease (-2%). In second place is Migros (2) with 16% (also with a slight decrease of -5%). In percentage terms, Procter & Gamble (3) and Swisscom (6) also significantly reduced traditional advertising pressure (-19% and -17% respectively) but have kept their places. Ferrero (4) and L’Oréal (5) also remain in the same positions despite slightly higher advertising pressure than in 2022 (+3% and +6% respectively).

On the other hand, the following four companies increased their investments in this area and have reaped the rewards in the ranking. Henkel (10) and Beiersdorf (8) have both risen 8 places compared to the previous year, while IKEA has jumped from 13th to 7th place and Galaxus has risen 3 places to make it into the top 10.

Jumbo has the largest percentage increase in the top 20 after its merger with Coop Bau+Hobby (+93%); this has catapulted the DIY company from 41st to 15th place. With increases nearing 40%, Unilever (16) and Nestlé (19) have both returned to the top 20. McDonald’s (11), Lidl (12), Denner (13), Interdiscount (14), Sunrise (17) and Aldi (20) reduced their traditional advertising pressure in 2023, with the first 5 losing their places in the top 10 and Aldi falling from 15th to 20th place. In percentage terms, Sunrise made the largest reduction (-36%).

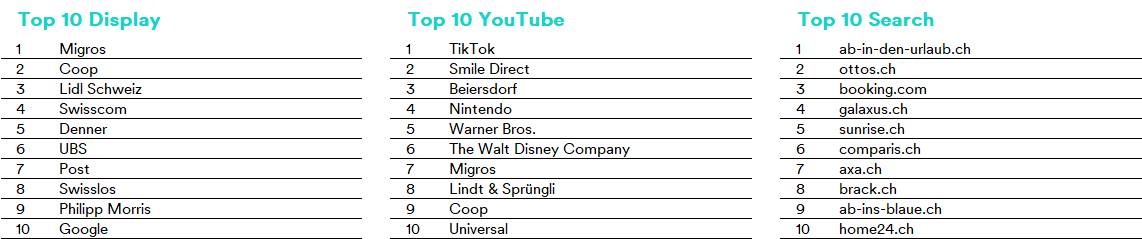

Retailers – especially Migros and Coop – are also the forerunners when it comes to display ads. Along with Lidl and Denner, there are 4 retailers in the top 10. Swisslos, Philipp Morris and Google are among the new companies to make it onto the list, alongside the Swiss “institutions” Swisscom, UBS and Post.

On YouTube, entertainment companies dominate the rankings, with TikTok taking the top spot and Nintendo, Disney and Universal featuring in the top 10. Putting in a surprisingly strong showing was Smile Direct, which comes in at 2nd place, ahead of Beiersdorf. Migros, Lindt & Sprüngli and Coop also made it into the top 10.

As more of a pull form of marketing than a push one, search offers ideal insights into the needs of the average Swiss citizen. What do we actually do online? We book trips: Ab-in-den-Urlaub.ch (1), booking.com (3), ab-ins-blaue.ch (9). We shop: ottos.ch (2), galaxus (4), brack.ch (8), home24.ch (10). And we compare prices: comparis (6). The brands Sunrise.ch and Axa.ch come in at places 5 and 7 respectively and are almost the odd ones out here.

Automotive sector gathers pace again in 2023

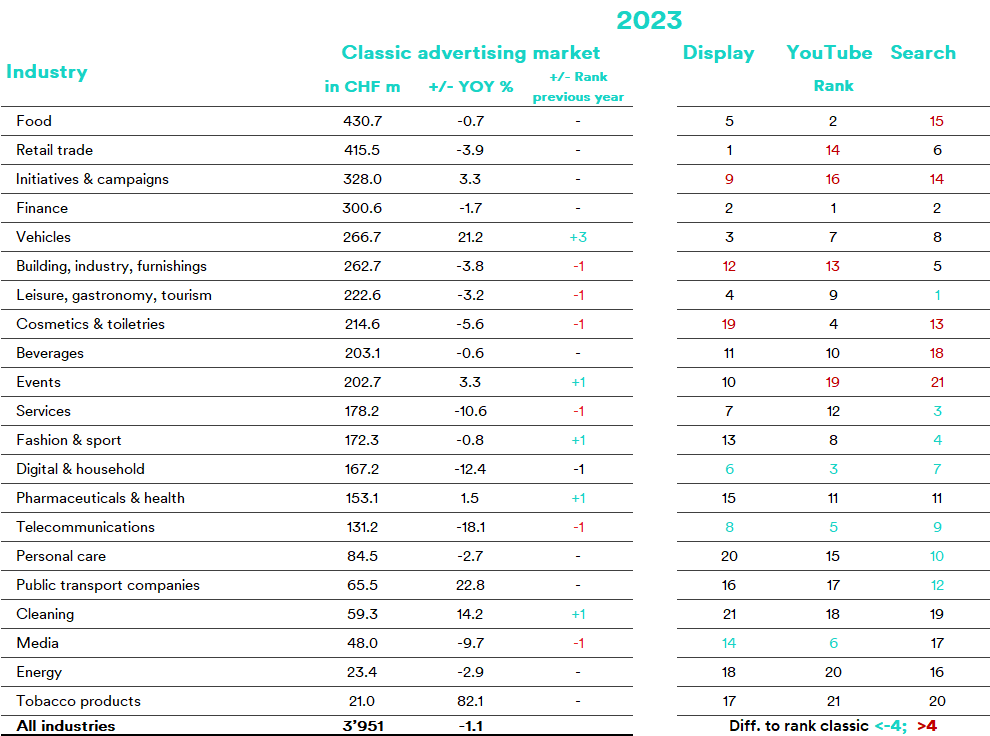

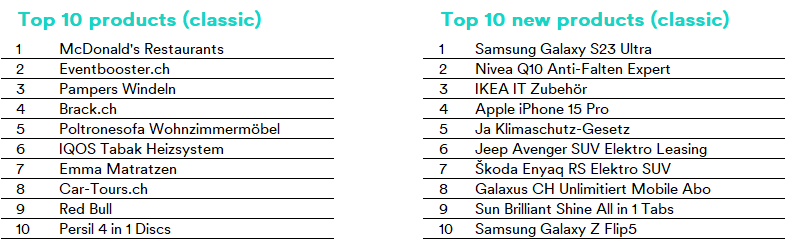

2023 was a year of celebration for the automotive sector. Embattled by the COVID-19 pandemic and supply bottlenecks, the sector grew by 21.2%, climbing 3 places to number 5. Jeep and Škoda each have a product in the top 10 of newly advertised products for 2023 – both products being electric SUVs.

The only sectors to outperform the automotive sector in percentage terms were transport operators (+22.8%) and tobacco products (+82.1%), with the latter also having a product in the top 10, namely the IQOS heated tobacco system. However, this did not lead to any changes in the pecking order, other than among events (+3.3%), pharmaceuticals and health (+1.5%), and cleaning (+14.2%). Fashion and sport profited from the traditionally defensive advertising behavior of the telecommunications sector (-18.1%) and climbed one place in spite of a minimal reduction (-0.8%).

The right-hand side of the table shows the online orientation of the sectors. The telecommunications sector, which came in at just position 15 in the traditional market, shone through when it came to display, YouTube and search ads (in turquoise); coming in at 8th, 5th and 9th respectively, they are more than 4 places higher than in the rankings for traditional channels.

There are no changes in the order of the top 4 sectors in the traditional sector ranking, although there are deviations in advertising pressure (-3.9% to 3.3%). Food stayed ahead of retail, initiatives and campaigns, and the finance sector, the latter enjoying high online rankings, with 2nd place for display and search ads and coming top for YouTube.

Summary and outlook

2023 marked a phase of consolidation and gradual change in the Swiss advertising market. Despite the slight decline in the traditional advertising market, the rise in specific areas, such as outdoor advertising, radio and cinema, reveals a diverse and adaptive market structure. The ongoing strengthening of online marketing channels, such as display and YouTube ads, emphasizes the growing significance of digital advertising strategies, even if the rate of growth flattened out compared to previous years.

Changes in search engine marketing – especially with Google – reflect the ever-changing nature of technologies and user behavior patterns. This prompts companies to continually adjust and optimize their online presence and their search engine strategies.

Major players such as Coop, Migros and P&G continue to dominate the traditional advertising market while other brands are moving up the rankings, showing how dynamic and competitive the market is. The strong presence of retailers when it comes to display ads and the dominance of entertainment companies in the YouTube ads rankings emphasize the varying strategic orientations across the different advertising channels.

The automotive sector is experiencing a comeback, which suggests that it is recovering from the blows dealt to it by the pandemic. The telecommunications sector’s presence in traditional and online media is an interesting discrepancy.

All in all, 2023 offers important insights into the changing priorities and strategies in play on the Swiss advertising market. If sectors want to succeed in what is a fast-changing digital ecosystem, adaptability and a willingness to innovate will continue to be of major importance going forward. It will be exciting to see whether they all manage it in 2024. Certainly, one positive aspect is that the advertising market in 2024 will, according to various market leaders, likely remain at around the same level as 2023.

Contact: mediafocus@mediafocus.ch, Tel.: +41 43 322 27 50

Annual review 2022