Highlights in May 2024

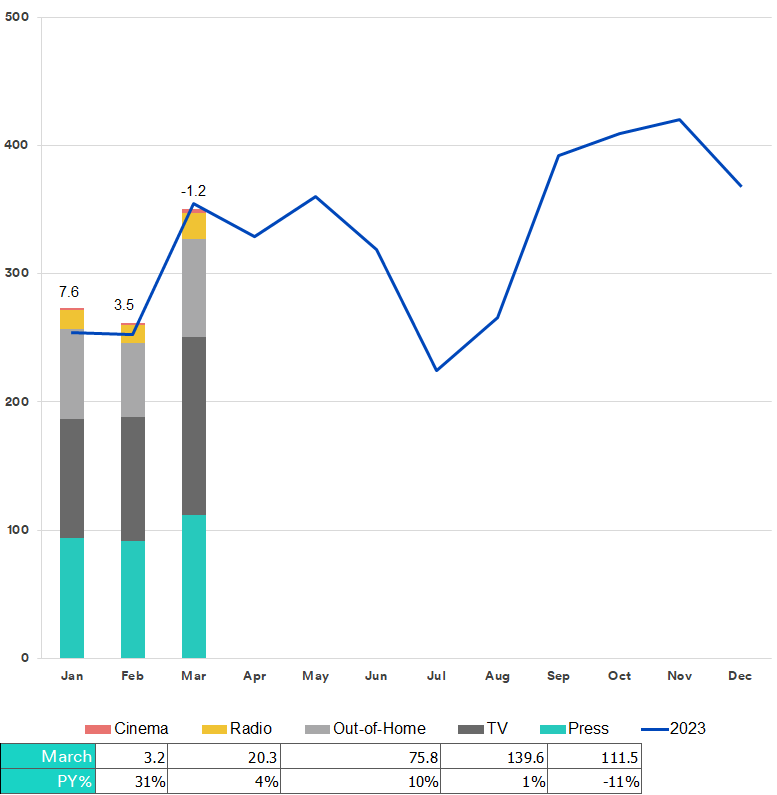

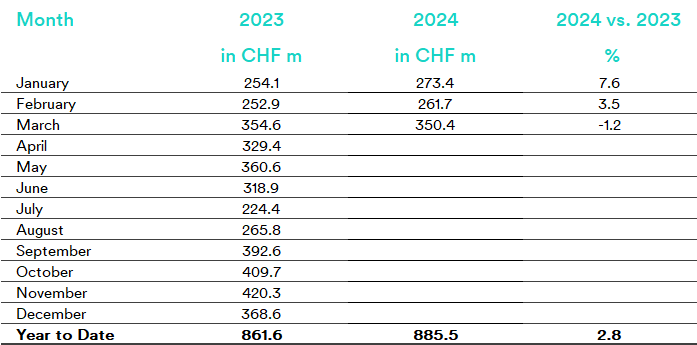

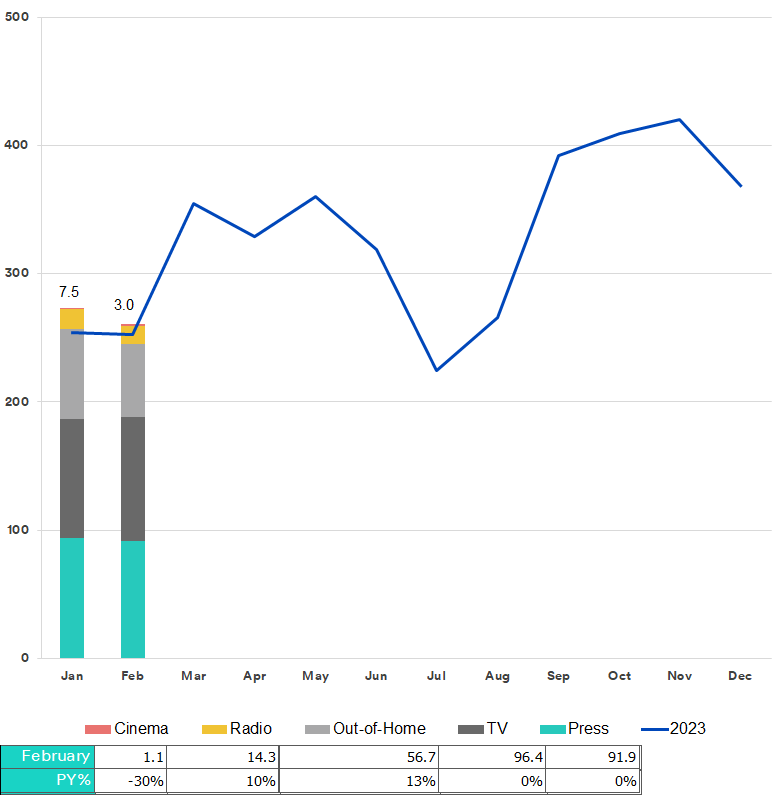

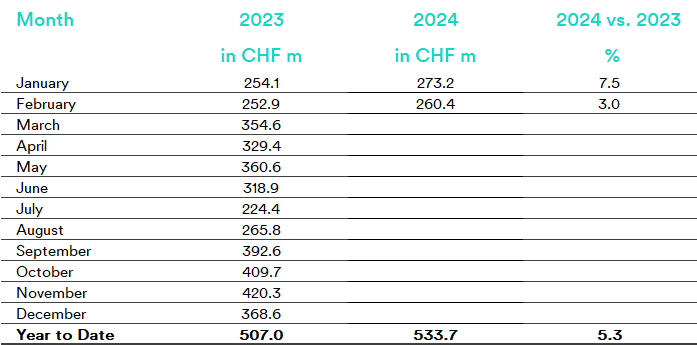

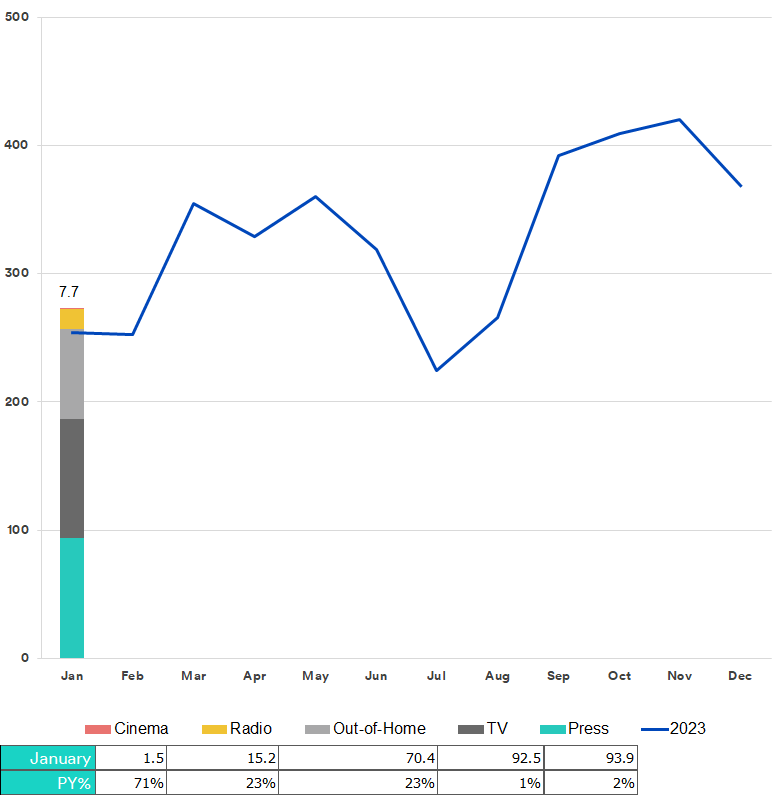

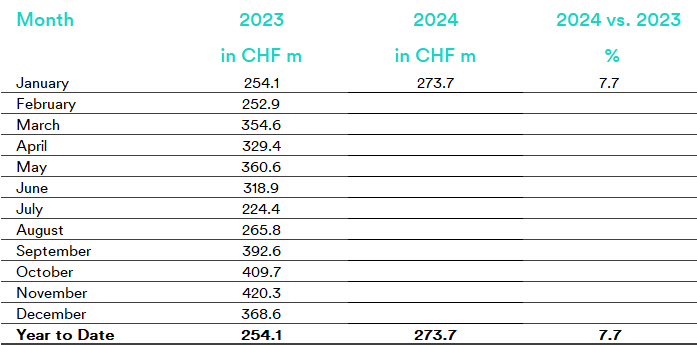

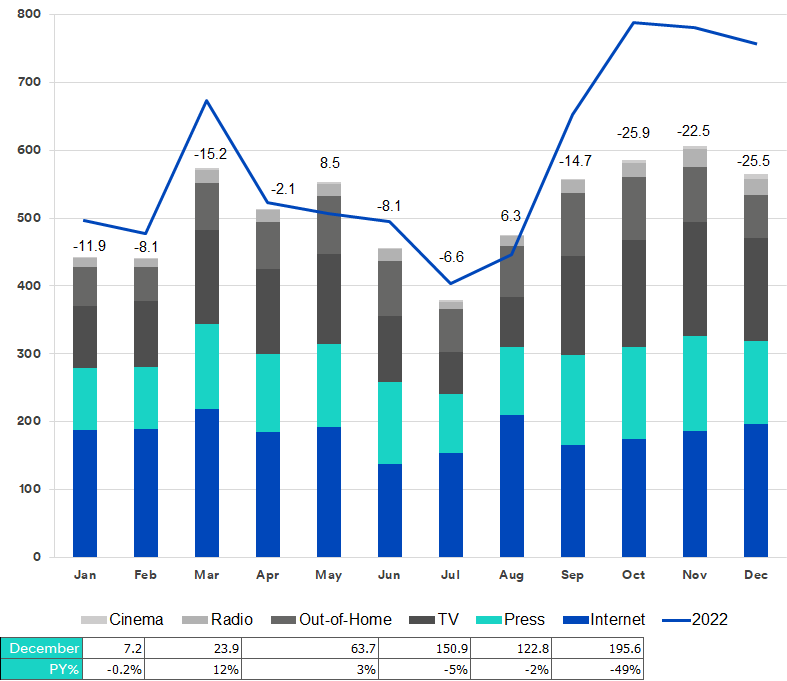

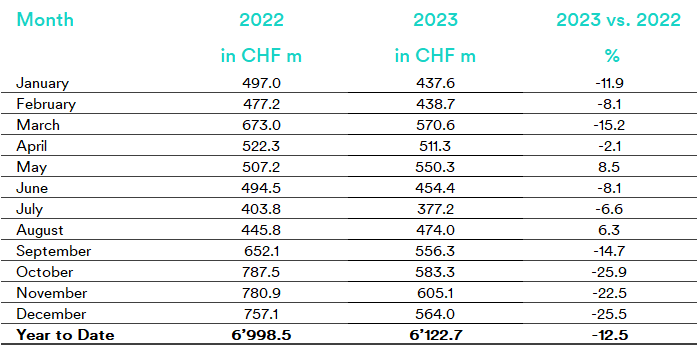

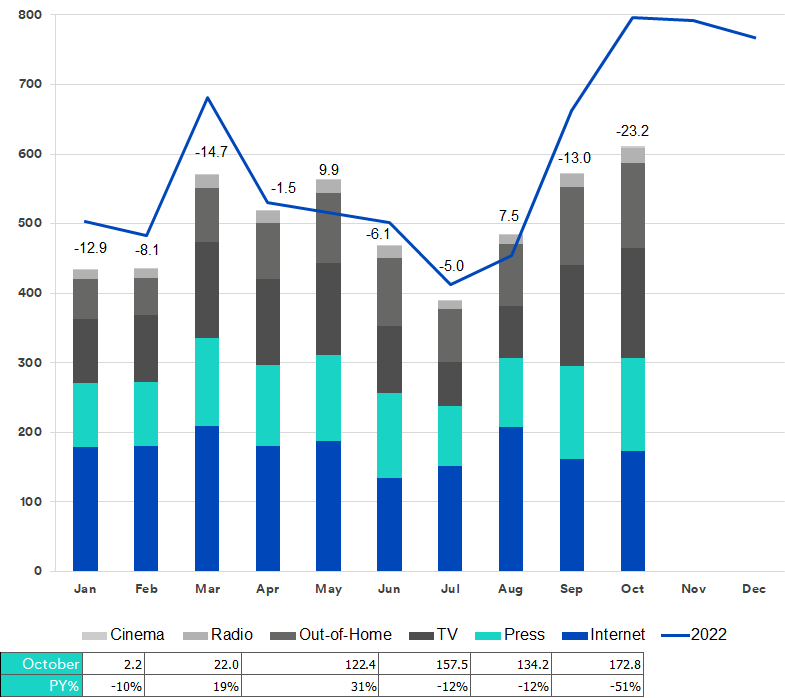

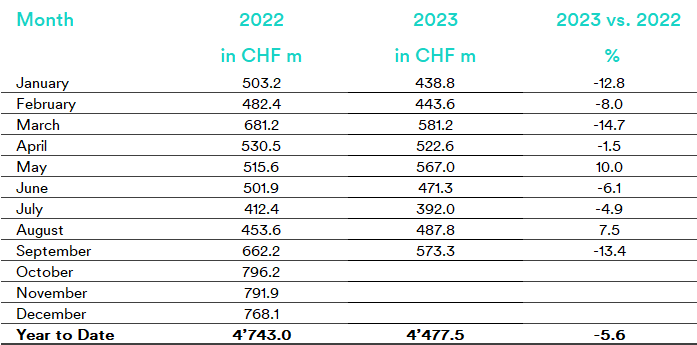

The “traditional” advertising market has been sitting around the CHF 350 million mark since March. The Swiss advertising market rose by a further 1.4% compared to April, and closed the month at CHF 352.0 million in advertising pressure. The advertising pressure for the first five months of the year was CHF 1,589.0 million. Although the advertising market in May was a little down on the previous year’s figure (-2.4%), it is slightly up YTD (+2.4%).

This boost in the media mix is primarily being driven by out-of-home advertising. Please note that the data from the marketer Livesystems is currently only available for 2024 (2023 is planned to be reintegrated along with the June data). Without taking Livesystems into account, the advertising market dropped by -4.2% in May and grew by +0.1% over the year as a whole.

It is clear that, apart from out-of-home advertising, all the other “traditional” media categories saw a decline in gross advertising revenue compared to the previous year. As in April, cinema fared the worst (-22%), closely followed by print with a drop of -11%. Radio (-4%) and TV (-2%) saw losses in the low single digits compared to the previous year.

In May, all media groups were left facing a decline in comparison to last year’s figures. In percentage terms, cinema fell the most (-22.4%), followed by print (-11.0%), radio (-3.7%) and TV (-2.5%). Out-of-home was the sole category in the black – both with (+11.0%) and without (+3.3%) Livesystems.

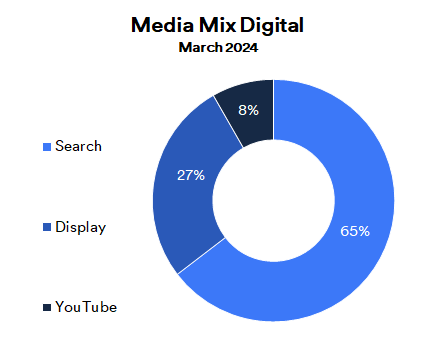

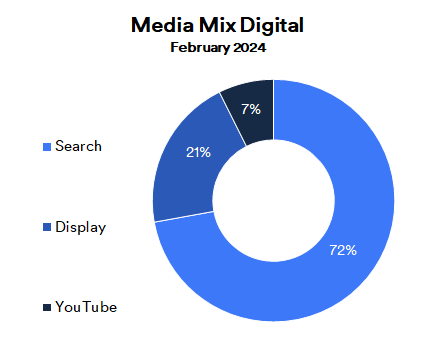

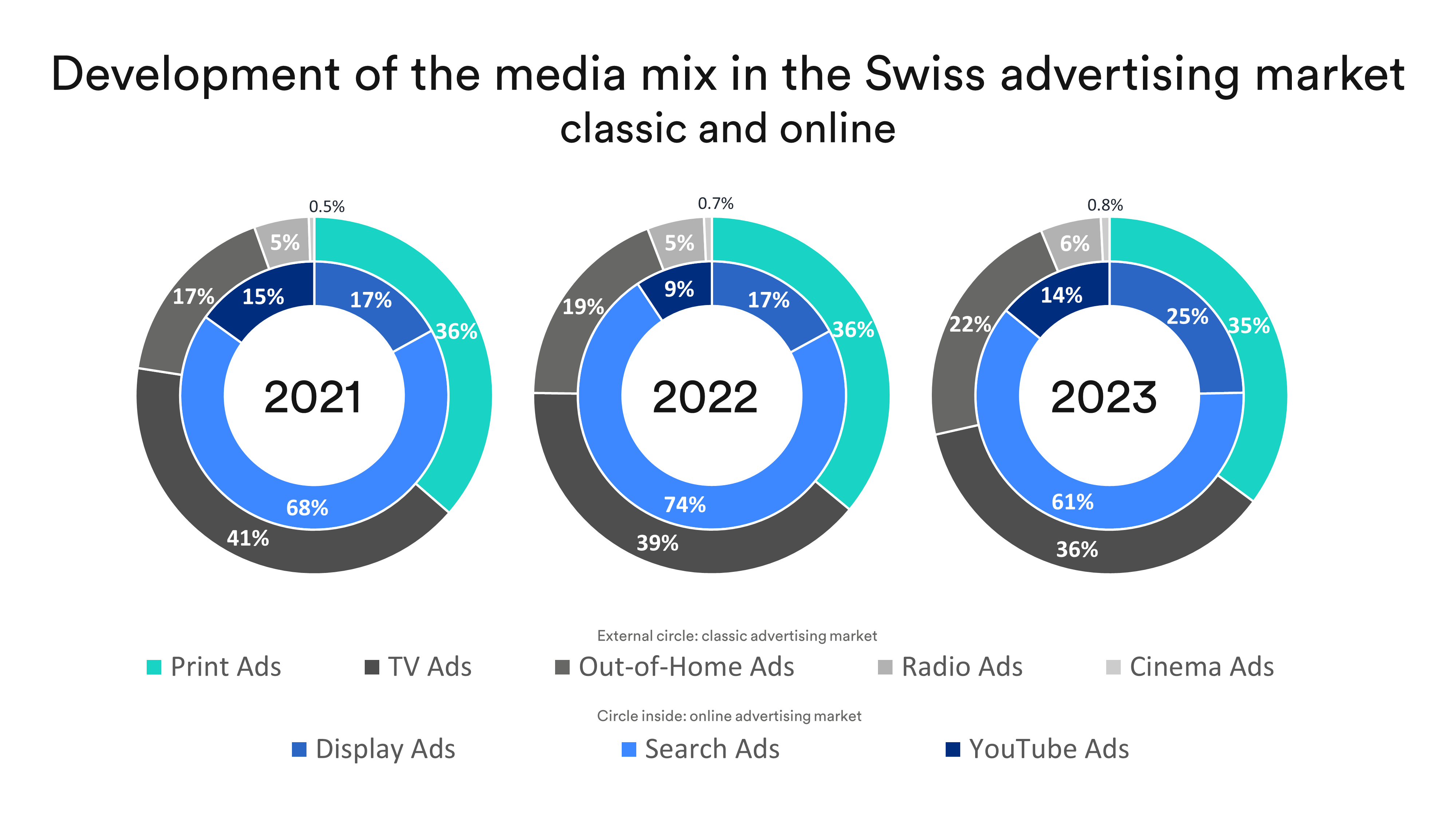

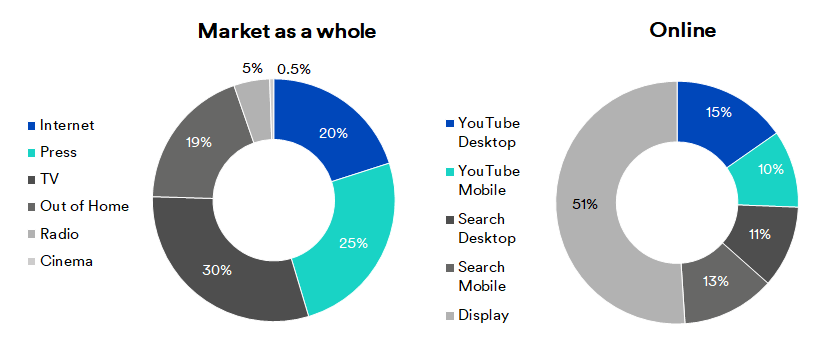

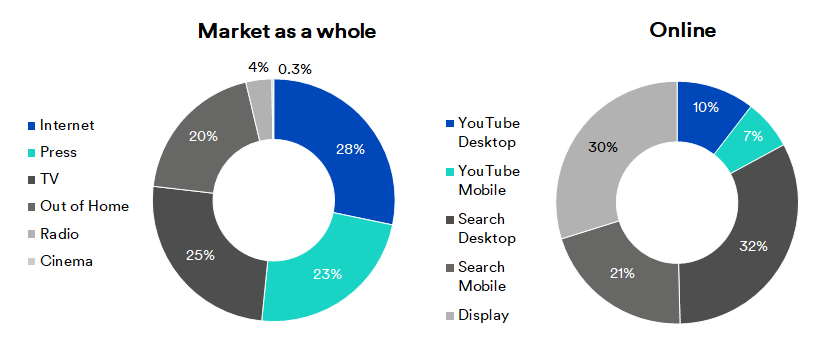

Search engine advertising took a bigger piece of the digital advertising pie, growing by 5 percentage points to reach 70%. At 23%, display advertising managed to hold on to second place, despite a slight decrease compared with last year (-4%), while YouTube was in close pursuit with a 9% jump.

From 2024, we will be reporting the traditional advertising market and digital channels (search, YouTube, display) separately to ensure better comparability to the previous year. Volatility in recording in the online sector, due to external influences such as adjustments made by Google, can lead to larger fluctuations throughout the year. In the search sector in particular there were numerous adjustments and changes made by Google in the last half of the year, which made comparing gross advertising spending with the previous year difficult.

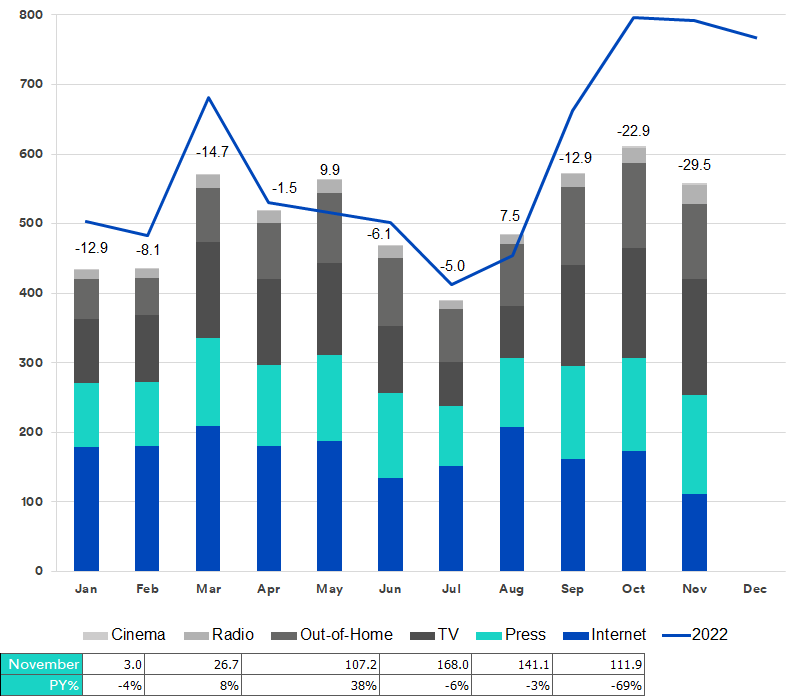

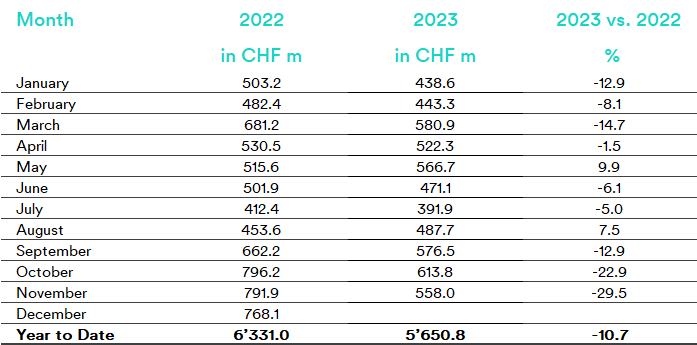

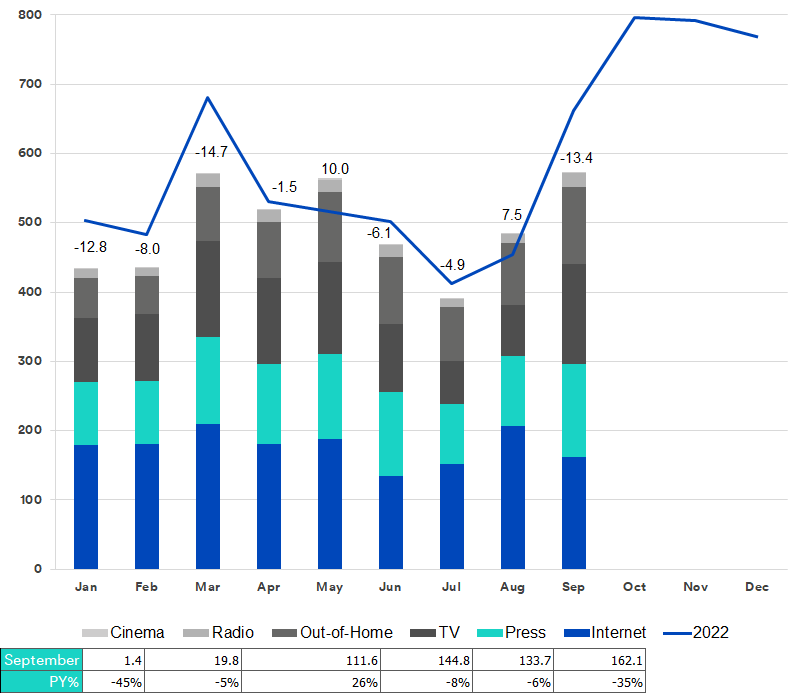

Advertising pressure in the market as a whole

Advertising pressure development up to May 2024 in CHF million gross.

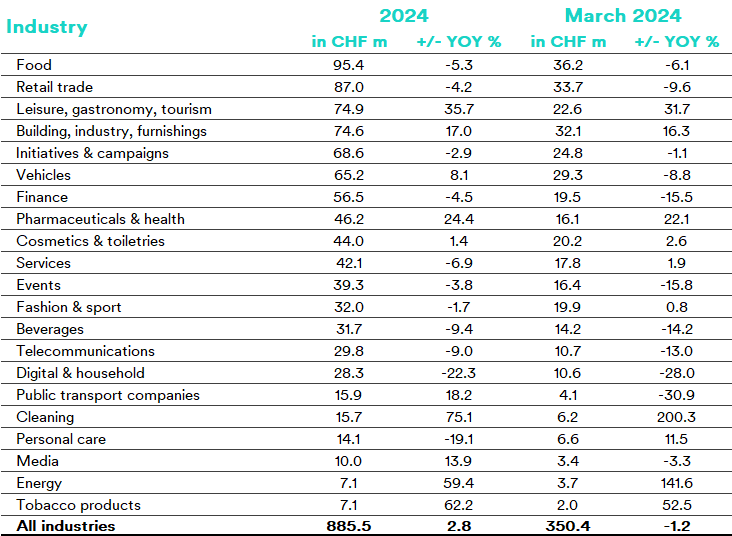

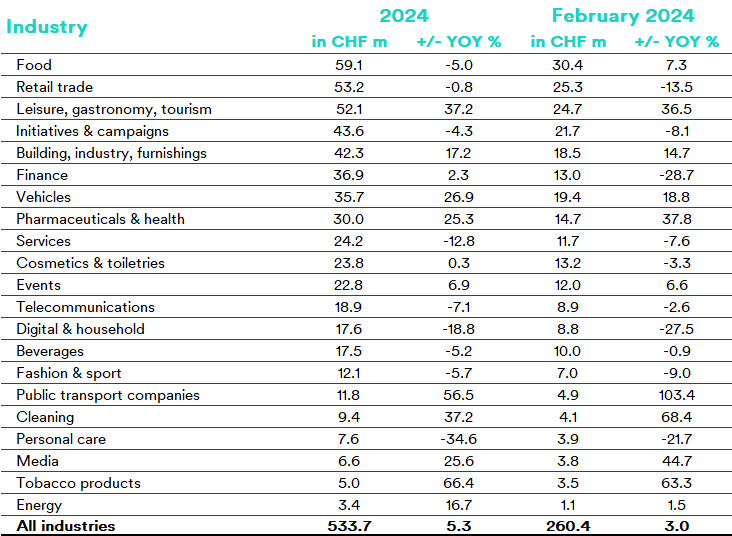

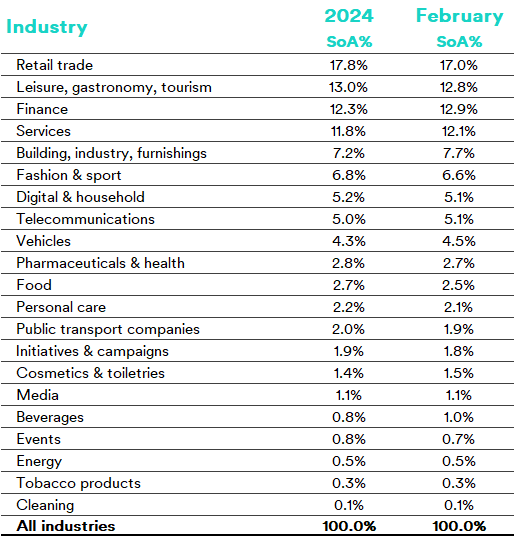

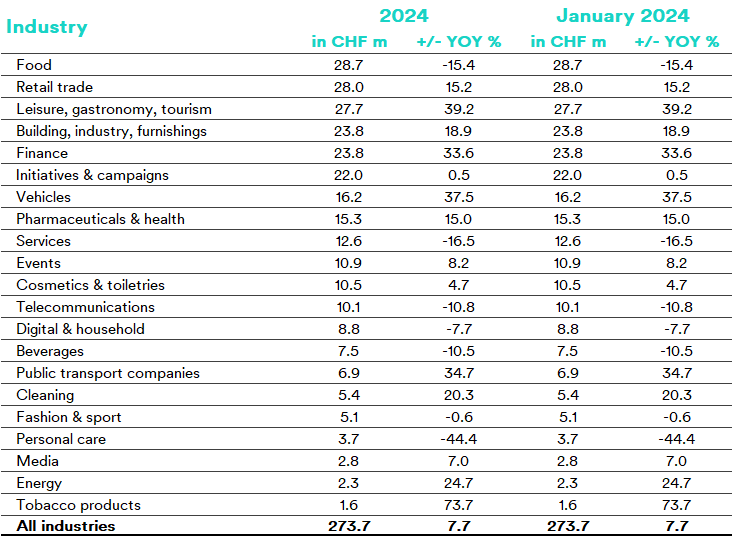

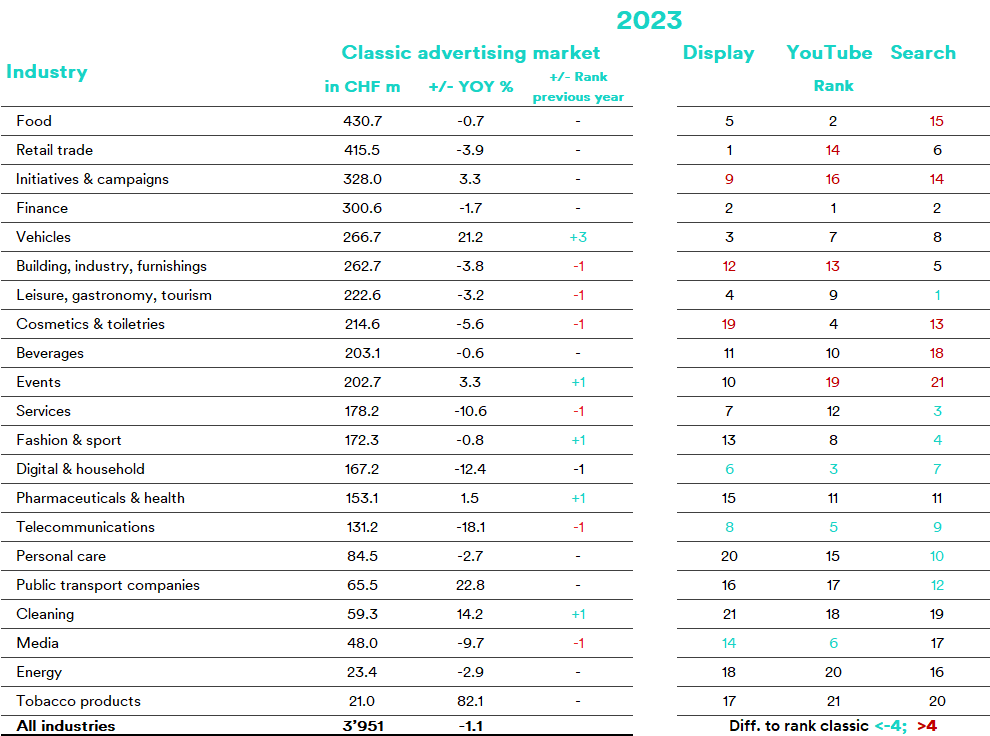

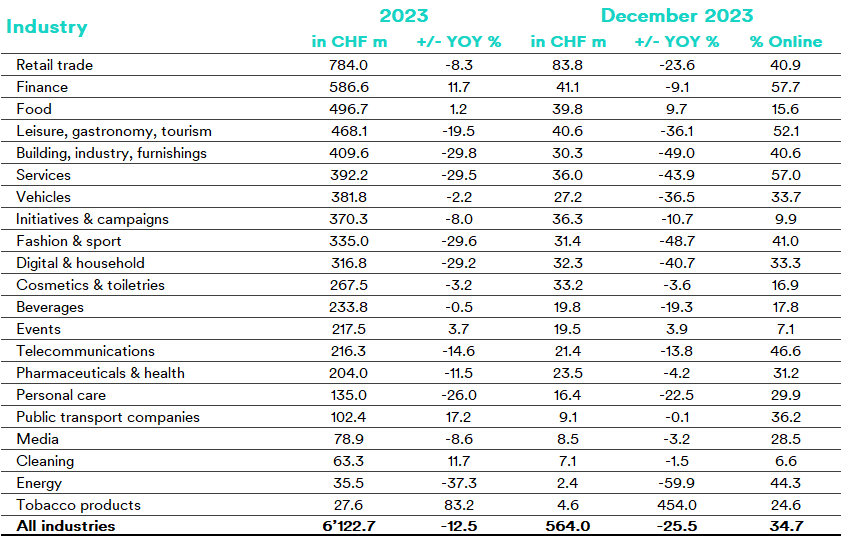

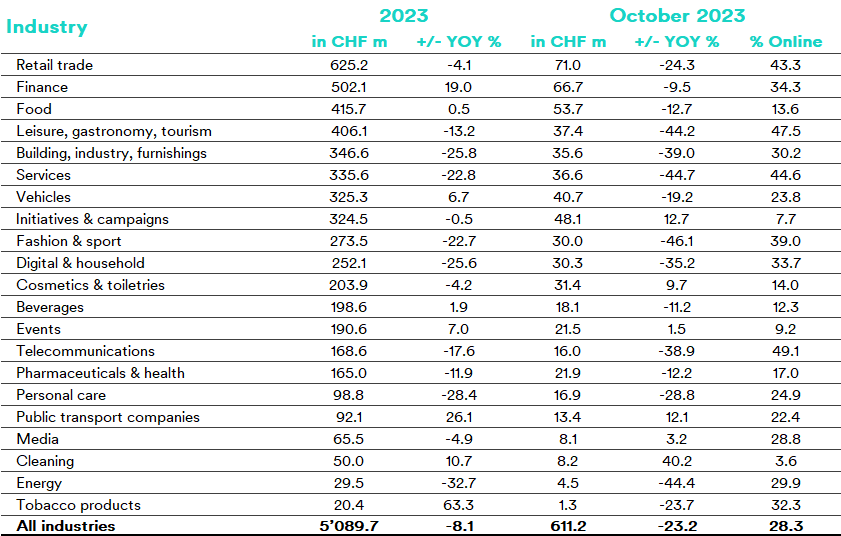

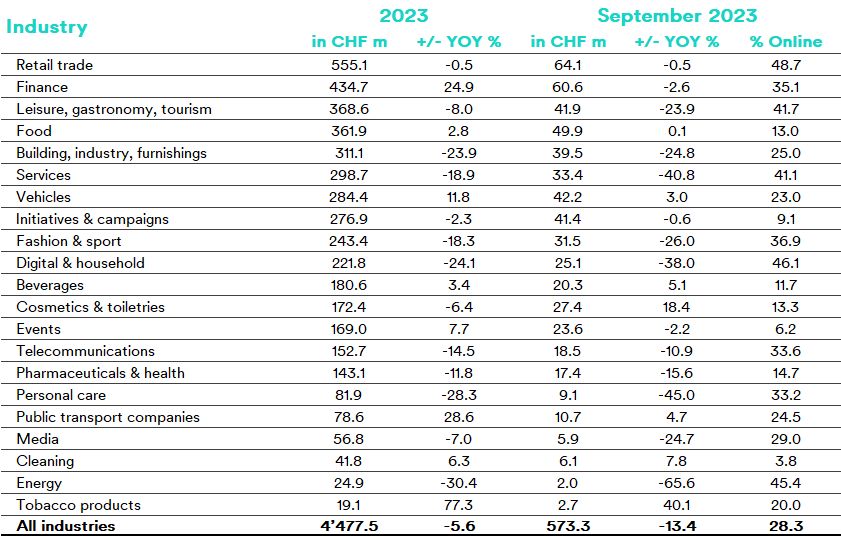

Low growth in individual sectors

Thirteen sectors saw growth in April – but just 8 out of 21 sectors enjoyed positive development in May compared to the previous year. The biggest upswing was generated by the cleaning (+73.8%) and cosmetics & toiletries (+60.5%) sectors, followed by construction, industry & furnishings (+14.9%), beverages (+10.9%), and leisure, gastronomy & tourism (+10.1%). The other three sectors recorded growth in the low single-digit range.

A decline in 13 sectors

All told, 13 sectors experienced negative growth compared to the previous year. Tobacco (-25.4%) and initiatives & campaigns (-24.0%) were the hardest hit. The remaining 11 sectors shrank by between -2.6% (energy) and -17.5% (retail and media).

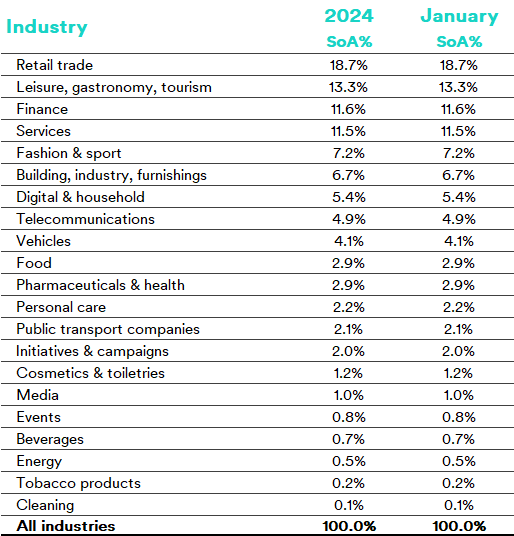

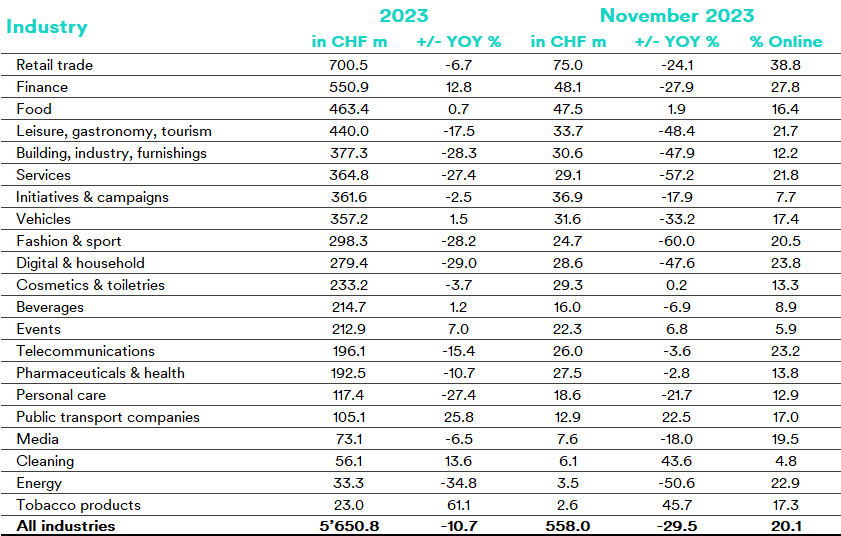

Sector ranking

Sector ranking in May.

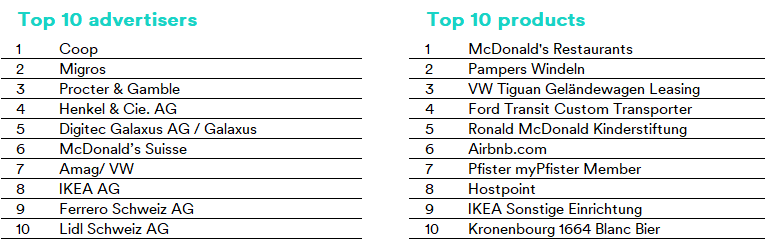

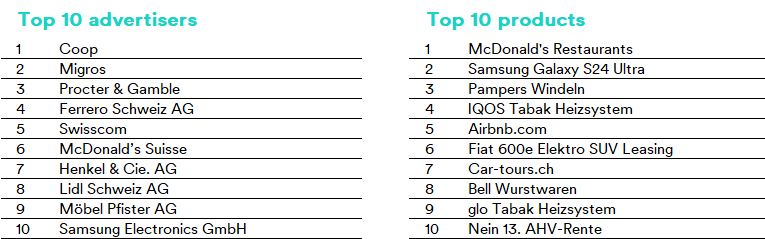

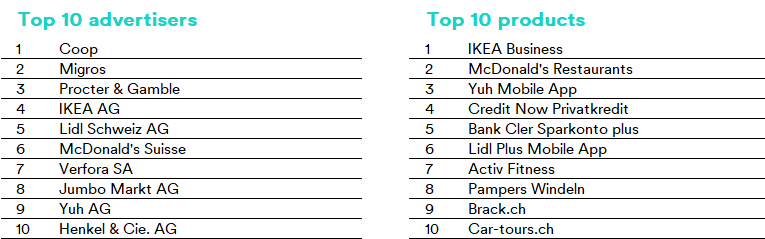

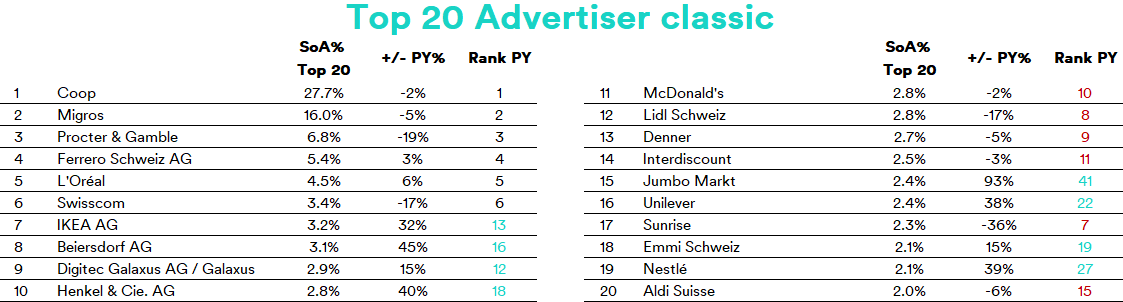

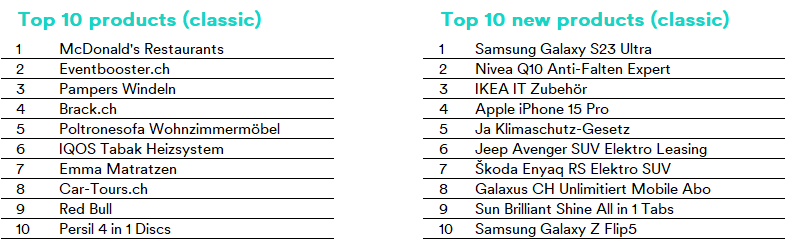

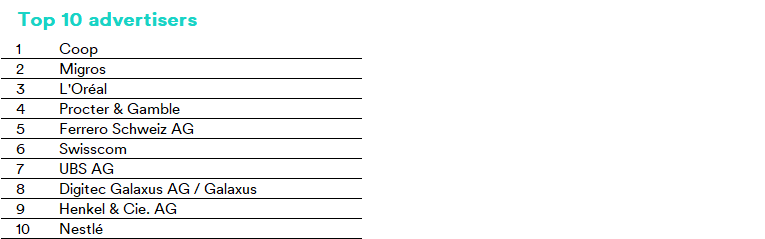

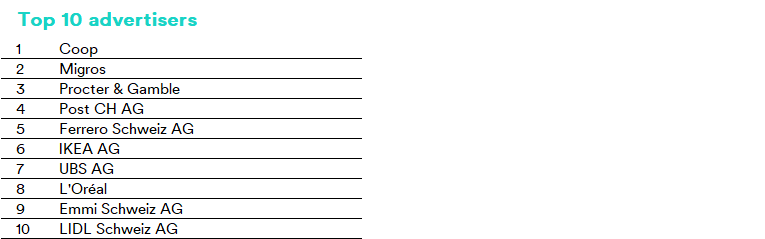

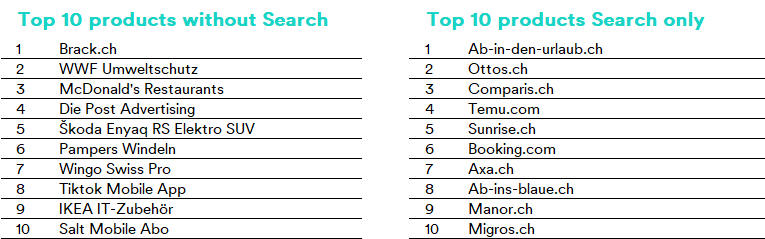

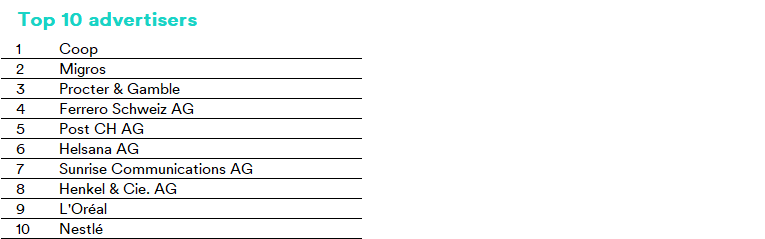

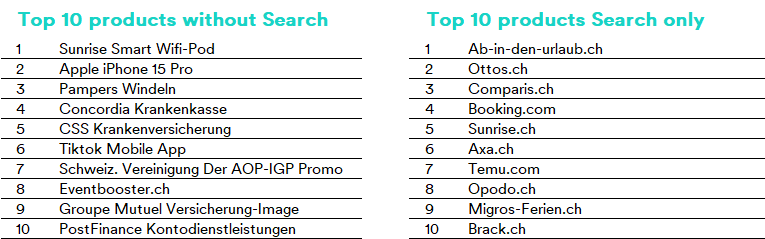

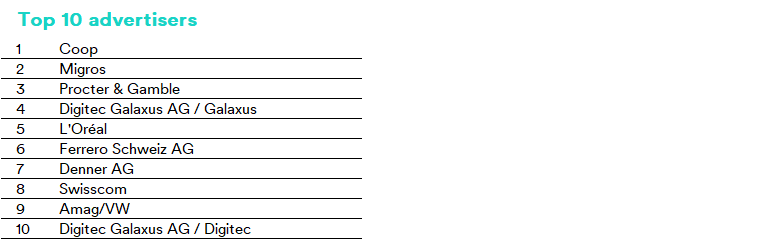

Top advertisers and products

The top advertisers and most advertised products and services (excluding range, image and other advertising) in May.

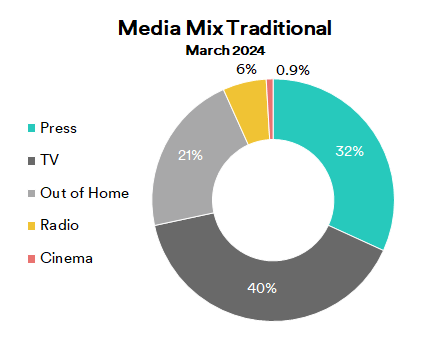

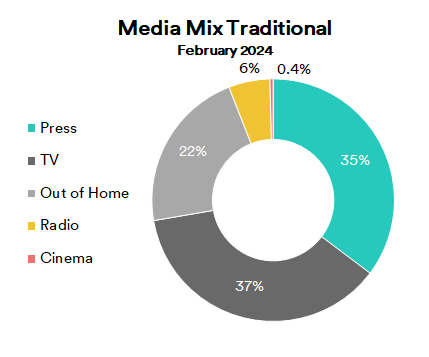

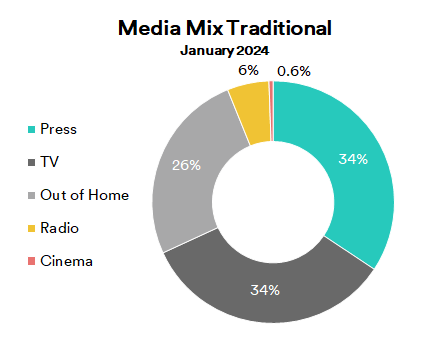

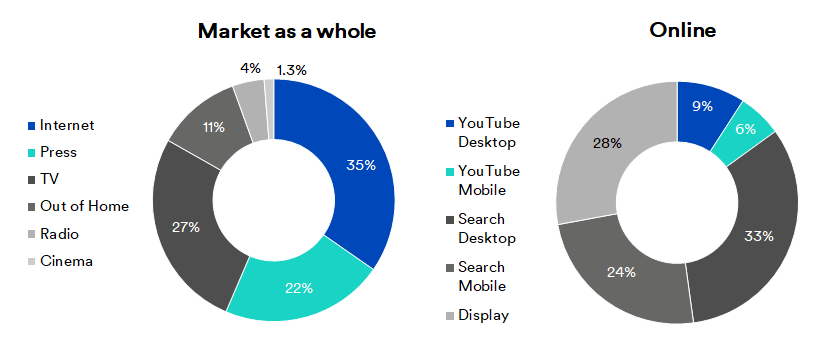

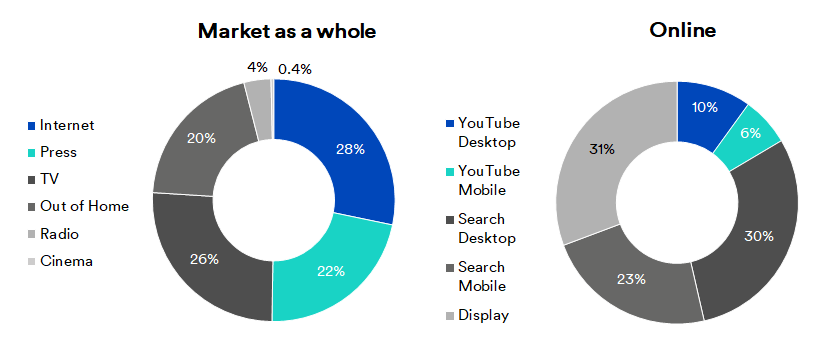

Media Mix

Media mix for May.

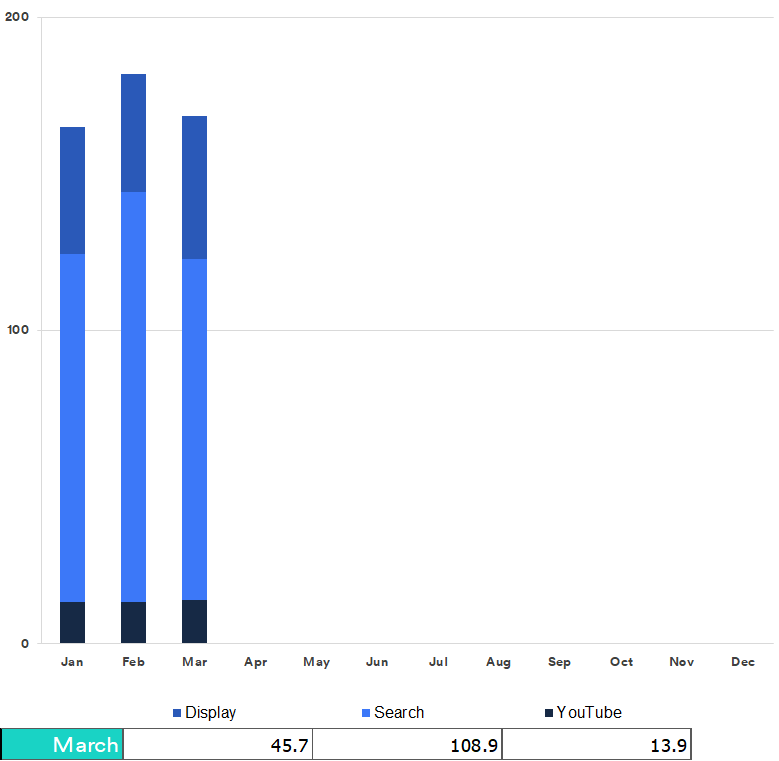

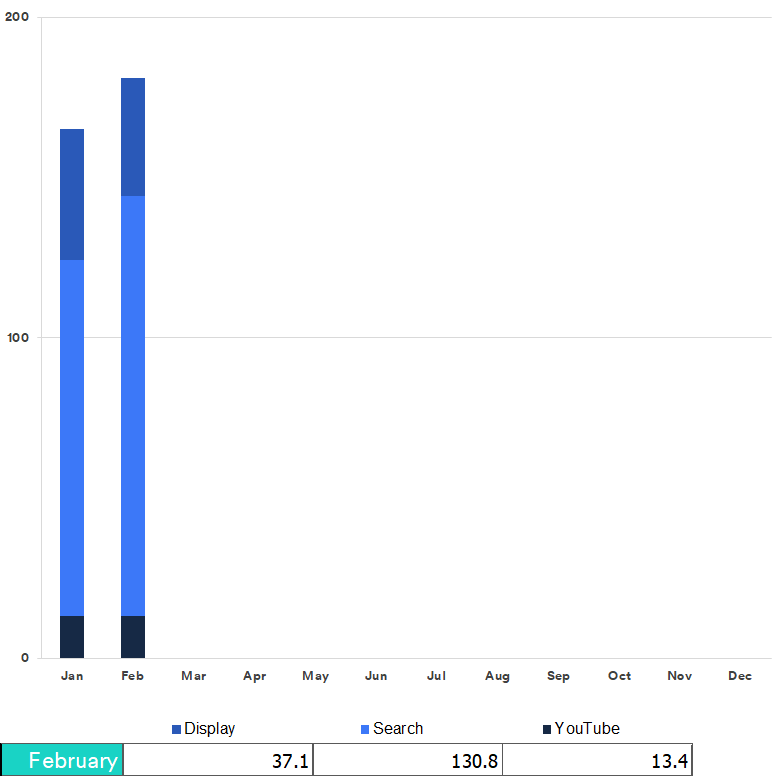

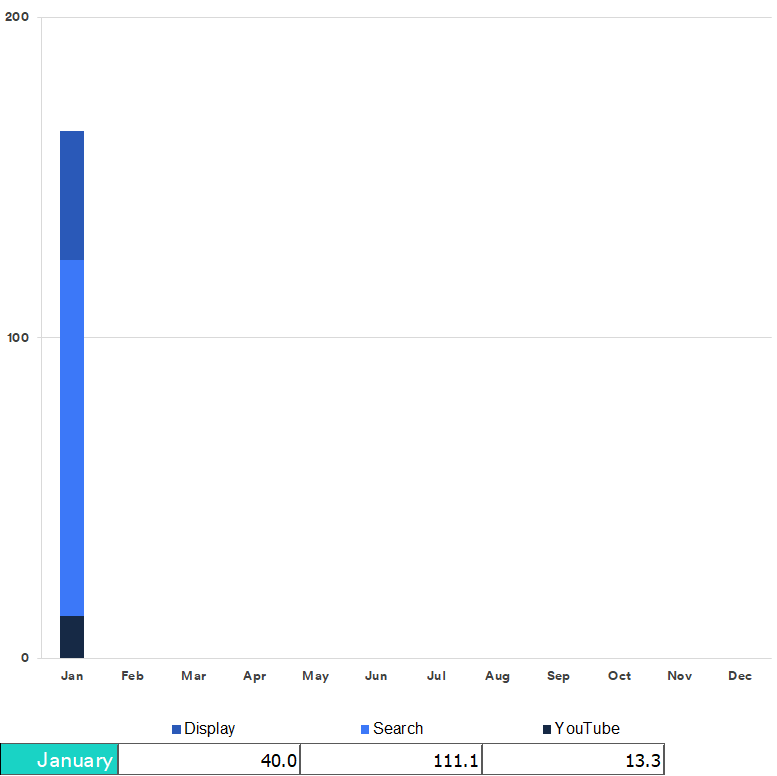

Advertising pressure in the digital market

Advertising pressure development up to May 2024 in CHF million gross.

Sector ranking: traditional vs. digital channels in comparison

The retail sector did very well in the “traditional” and digital markets alike during April and May, taking second place in both. It even tops the leaderboard for the digital market YTD. The finance and leisure, gastronomy & tourism sectors are hot on its heels, taking second and third place in the digital market. These two sectors were also on a strong footing in the “traditional” market, occupying positions six and four respectively.

The food sector took first place in the “traditional” market, while the construction, industry & furnishings sector is in third place YTD. The pair have each fallen one place in the digital market rankings since April and are now 11th and 6th respectively.

The cleaning sector is similarly performing better in the “traditional” market: it holds 16th place here, but is bringing up the rear in the digital space.

Sector ranking

Sector ranking in May.

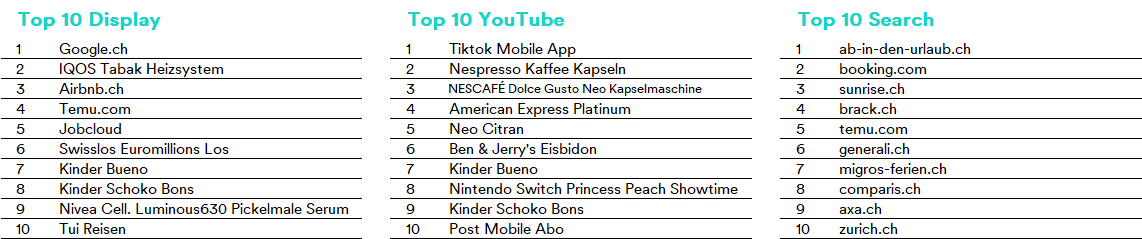

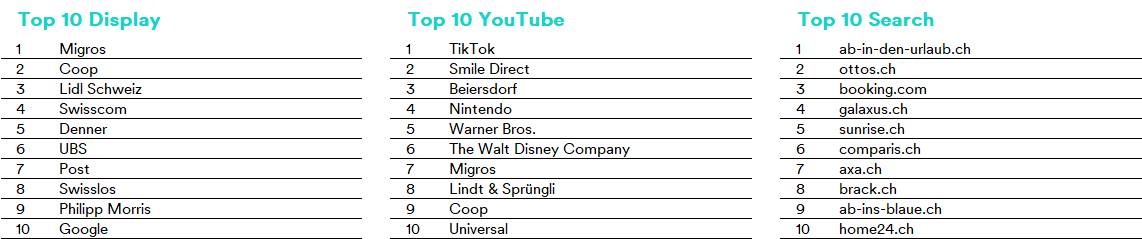

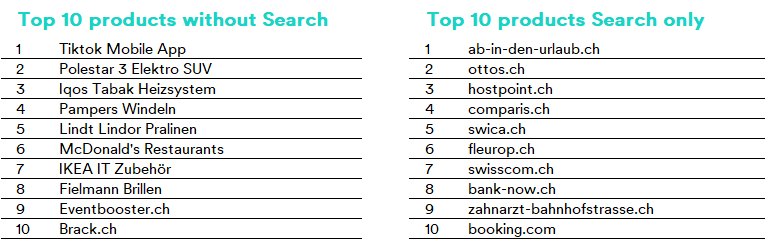

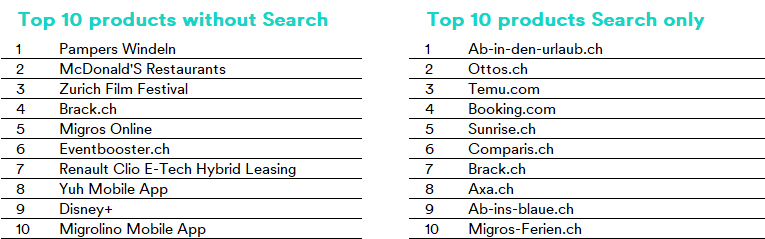

Top digital products

The most advertised products and services (excluding range, image and other advertising) in May.

The products “taten-statt-worte.ch” and “temu.com” took the top two spots for display advertising. As in April, “TikTok mobile app” topped the table for YouTube, followed by “temu.com”. For search, “sunrise.ch” was in the lead (as in April), then “zurich.ch”.

The only product to make it into the top ten across all three media groups was the Chinese e-commerce heavyweight “temu.com”. “temu.com” took second place for display and YouTube, and eighth place for search.

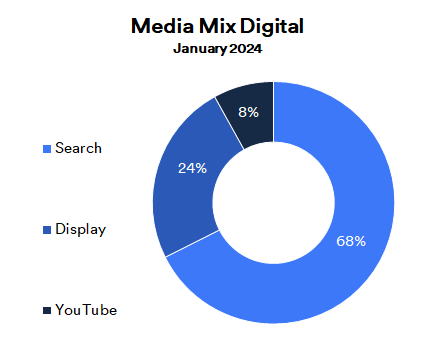

Media Mix

Media mix for May.

Contact: mediafocus@mediafocus.ch, Tel.: +41 43 322 27 50

Annual review 2023 Advertising Market Trend April 2024 Factsheet Media